The upcoming U.S. presidential election, set for November 5, 2024, is expected to have profound implications for the economy and financial markets.

The race, featuring Donald Trump for the Republican Party and Kamala Harris for the Democratic Party, has investors closely watching each candidate’s policy stance, as their win could influence tax rates, regulatory landscapes, and fiscal policies.

In this post, we’ll explore historical election impacts, candidate profiles, winning odds, and the asset classes that may benefit under each candidate’s leadership.

Historical Impact of Elections on Financial Markets

Historically, U.S. presidential elections bring about market volatility and, in some cases, long-lasting shifts in market sentiment.

The stock market tends to perform differently based on the winning party and the subsequent policy shifts.

2008 Election (Obama vs. McCain): The financial crisis heavily influenced the 2008 election, and Obama’s win led to mixed reactions in the short term. However, his administration’s introduction of stimulus packages helped stabilize the economy, and the S&P 500 experienced a steady climb over the next several years.

2016 Election (Trump vs. Clinton): The unexpected Trump victory led to a rapid market rally. Known as the “Trump Rally,” the S&P 500 surged by approximately 25% in the following year, fueled by pro-business policies, tax cuts, and deregulation.

2020 Election (Biden vs. Trump): Amid the pandemic, Biden’s focus on infrastructure and renewable energy investment gave certain sectors a boost. However, his administration’s regulatory approach in technology and energy sectors introduced some volatility.

Data shows that markets often exhibit volatility before and after election days, with equities tending to recover and stabilize once results are confirmed.

When the incumbent party wins, markets generally rally, while a change in power brings a cautious approach from investors.

Brief Background of Each Candidate and Their Key Policies

Donald Trump (Republican):

Background: Former President Donald Trump previously served from 2017 to 2021. Known for his business-first approach, he has emphasized economic growth through deregulation, tax cuts, and “America First” trade policies.

Key Policies:

Energy: Favors traditional energy sources, aiming to support oil, natural gas, and coal industries through deregulation.

Defense and National Security: Advocates for increased military spending and a robust national security framework.

Deregulation and Tax Cuts: Prioritizes corporate tax cuts and reduced regulatory burdens on businesses, particularly in finance and real estate.

Trade Policy: Emphasizes protectionism, with a strong stance on tariffs, especially regarding U.S.-China trade.

Kamala Harris (Democrat):

Background: Vice President Kamala Harris has a background in law and has supported progressive initiatives, including healthcare expansion, renewable energy investment, and climate-friendly infrastructure projects.

Key Policies:

Climate and Green Energy: Aims to increase investments in renewable energy, with incentives for solar, wind, and clean technologies.

Healthcare Access: Supports expanding healthcare access and reducing healthcare costs, including potential drug pricing reforms.

Infrastructure: Advocates for sustainable infrastructure, focusing on green construction and modernization of public transportation.

Technology and Innovation: Promotes tech innovation, cybersecurity, and digital access, along with a stronger regulatory framework for tech giants.

Odds of Each Candidate Winning

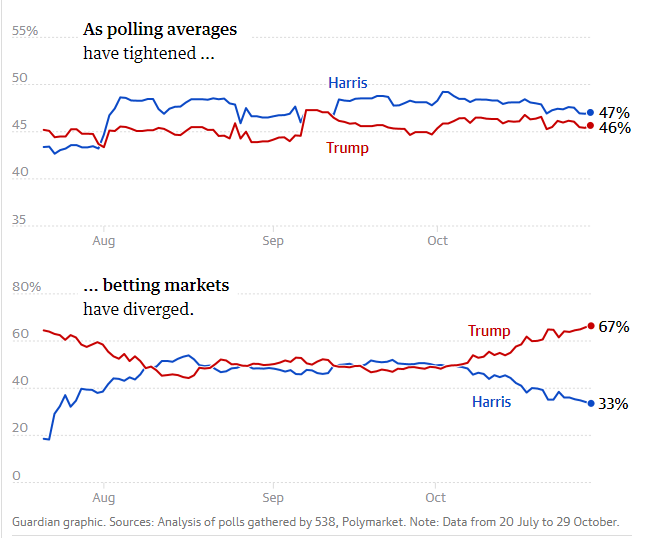

This election is shaping up to be one of the tightest races in recent history, with official polls indicating a neck-and-neck competition between Kamala Harris and Donald Trump. While traditional polls suggest a close contest, Trump and his supporters have pointed to alternative sources—particularly betting markets—that project him as the frontrunner. Trump recently cited these “gambling polls,” claiming they show him with a substantial lead, even stating figures like 65% to 35% in his favor at a campaign event.

Several popular betting platforms indeed reflect this sentiment. As of recent data:

Polymarket, a prominent election betting service, currently puts Trump’s chances of winning at 67% and Harris’s at 33%.

Kalshi, another major platform, shows similar odds, giving Trump 62% and Harris 38%.

With trust in traditional media and polling declining, betting platforms have gained traction as alternative “predictive” tools, with some public figures, including Elon Musk, suggesting that these markets might be more reliable indicators. Unlike poll respondents who often answer based on preference, those betting on outcomes are motivated by profit and thus tend to focus on who they think will actually win rather than who they hope will prevail.

Betting Market Trends and Potential Biases: Interest in betting on the 2024 election is reportedly higher than ever, driven by the widespread legalization of sports betting and recent legal victories for platforms like Kalshi. Some, however, have raised concerns over the potential for market manipulation. Reports indicate that a single French national placed roughly $28 million worth of bets on Trump across four accounts on Polymarket. Although this activity has been labeled as “personal views” rather than manipulation, the absence of strict betting limits could allow wealthy individuals to skew the odds in favor of their preferred candidate.

Regulatory Scrutiny: The rise of election betting has not gone unnoticed by regulators. The Commodity Futures Trading Commission (CFTC) has attempted to shut down or restrict several platforms, citing concerns over unregulated political betting markets. However, Kalshi recently won a legal battle that permits it to take U.S. bets on election outcomes, a ruling that may pave the way for further growth in election betting.

While official polls continue to portray a tight race, betting markets currently lean toward Trump as the favorite, with Trump’s campaign embracing this narrative. As betting markets and traditional polls offer differing views, investors and observers remain divided on which source may ultimately prove more predictive.

Asset Classes Likely to Benefit if Each Candidate Wins

If Donald Trump Wins:

Energy and Fossil Fuels: Trump’s support for traditional energy likely favors oil, gas, and coal sectors. Investors may gain exposure through ETFs like XLE (Energy Select Sector SPDR), which holds major oil and gas companies.

Defense and Aerospace: Increased defense spending would benefit aerospace and defense contractors such as Lockheed Martin and Raytheon. ETFs like ITA (iShares U.S. Aerospace & Defense ETF) could offer broad sector exposure.

Financial Services: With Trump’s pro-deregulation stance, large financial institutions may see increased profitability. ETFs like XLF (Financial Select Sector SPDR) and KBWB (Invesco KBW Bank ETF) offer access to major banks and financial stocks.

Real Estate and Infrastructure: Real Estate Investment Trusts (REITs) may benefit from favorable tax policies. Look into REIT-focused ETFs like VNQ (Vanguard Real Estate ETF) for broader exposure, particularly in commercial real estate.

Industrial Metals: A continuation of protectionist policies could favor domestic steel and aluminum producers. Consider SLX (VanEck Vectors Steel ETF) to gain exposure to steel companies that would benefit from tariffs and support for heavy industry.

If Kamala Harris Wins:

Renewable Energy and ESG Investments: Harris’s focus on green energy would likely boost clean energy companies. ETFs like ICLN (iShares Global Clean Energy ETF) or TAN (Invesco Solar ETF) offer direct exposure to renewable energy stocks.

Healthcare and Biotechnology: Harris’s stance on healthcare access could benefit managed care providers and biotech firms focused on affordable healthcare. XLV (Health Care Select Sector SPDR) and IBB (iShares Nasdaq Biotechnology ETF) are options for healthcare exposure.

Green Infrastructure: Companies involved in eco-friendly construction and infrastructure may gain from Harris’s policies. Infrastructure ETFs like PAVE (Global X U.S. Infrastructure Development ETF) could be a way to access companies expected to benefit from sustainable projects.

Technology and Innovation: Increased emphasis on tech infrastructure, 5G, and cybersecurity may support growth for technology companies. QQQ (Invesco QQQ ETF) provides exposure to the Nasdaq 100, with high concentrations in tech firms.

Commodities for Green Tech: Harris’s renewable push would increase demand for lithium, copper, and other materials used in green technologies. LIT (Global X Lithium & Battery Tech ETF) offers exposure to lithium and battery producers, while COPX (Global X Copper Miners ETF) focuses on copper.

The 2024 election could steer financial markets in distinct directions based on the victor’s policy focus.

Trump’s administration would likely prioritize traditional industries and a deregulated business environment, benefiting sectors like fossil fuels, defense, and financials.

Harris’s administration, on the other hand, would champion renewable energy, healthcare reform, and sustainable infrastructure, presenting opportunities in clean energy, ESG investments, and green technologies.

For investors, understanding these dynamics can inform strategic portfolio adjustments ahead of the election.

While each candidate’s policies may initially drive market volatility, focusing on diversified asset exposure aligned with either candidate’s strengths can help manage risks and capitalize on opportunities in a changing economic landscape.

As we come to the end of the blog post, here are some questions to ponder about:

How much weight should investors place on betting markets compared to traditional polls, and could this shift signal a broader change in how we interpret political forecasts?

In an era of increasing political polarization, how can investors best prepare for the potential market volatility and policy swings that come with close and contentious elections?

With significant differences in each candidate’s approach to key issues like energy, technology, and healthcare, how might this election reshape America’s economic priorities—and what could this mean for the future of sustainable and responsible investing?

https://synapsetrading.com/wp-content/uploads/2019/10/logo.jpg00Spencer Lihttps://synapsetrading.com/wp-content/uploads/2019/10/logo.jpgSpencer Li2024-11-02 00:38:132024-11-11 00:59:12The 2024 U.S. Presidential Election: What to Buy if Donald Trump or Kamala Harris Wins?

In times of economic uncertainty, central banks often turn to interest rate cuts as a key monetary policy tool to stimulate growth.

These cuts lower the cost of borrowing, encouraging individuals and businesses to take out loans, invest, and spend, which in turn supports economic expansion.

However, the implications of rate cuts extend far beyond basic borrowing; they ripple through financial markets, affecting asset prices, consumer confidence, and even international trade.

Understanding the dynamics of interest rate cuts is crucial for investors seeking to make informed decisions in an evolving economic landscape.

This blog post explores the concept of interest rate cuts, providing an in-depth analysis of their historical timeline and impact across various asset classes.

By examining past trends, we can better understand how rate cuts have influenced markets such as real estate, bonds, equities, and currencies.

Additionally, this report identifies potential investment opportunities that may arise from future rate adjustments, allowing investors to position themselves strategically in anticipation of further changes in the global financial environment.

As central banks around the world, including the Federal Reserve, continue to adjust interest rates to navigate economic challenges, investors must remain vigilant in evaluating how these changes influence the broader market.

From identifying sectors that benefit from lower borrowing costs to understanding how rate cuts can affect currency values and inflation, this report offers valuable insights into the role of interest rate policy in shaping investment opportunities over the coming years.

1. What are Interest Rate Cuts?

Interest rate cuts are a core component of a central bank’s monetary policy toolkit, primarily used to stimulate economic activity by reducing the cost of borrowing.

In the U.S., the Federal Reserve (Fed) manages the federal funds rate, the key rate at which banks lend to each other overnight to meet reserve requirements.

This rate serves as a benchmark for many other interest rates across the economy, such as those on mortgages, auto loans, and business financing.

By lowering the federal funds rate, the Fed aims to reduce borrowing costs across the economy, encouraging consumer spending and business investments, which in turn boosts economic growth.

The Mechanics of Interest Rate Cuts

When the Fed cuts interest rates, it increases the availability of money in the economy.

By reducing the cost of borrowing, businesses find it more affordable to finance expansion, purchase new equipment, or hire additional workers.

Consumers, too, benefit from lower interest rates on loans, mortgages, and credit cards, encouraging them to spend on homes, cars, and other goods.

This injection of capital into the economy typically spurs demand, leading to higher levels of economic activity.

The central bank cuts interest rates in response to a variety of economic challenges.

For example, during periods of recession, deflationary pressures, or weakening employment markets, rate cuts are used to ease financial conditions and prevent further economic contraction.

The ultimate objective is to stimulate growth, keep inflation within a target range (often around 2% for the Fed), and stabilize employment.

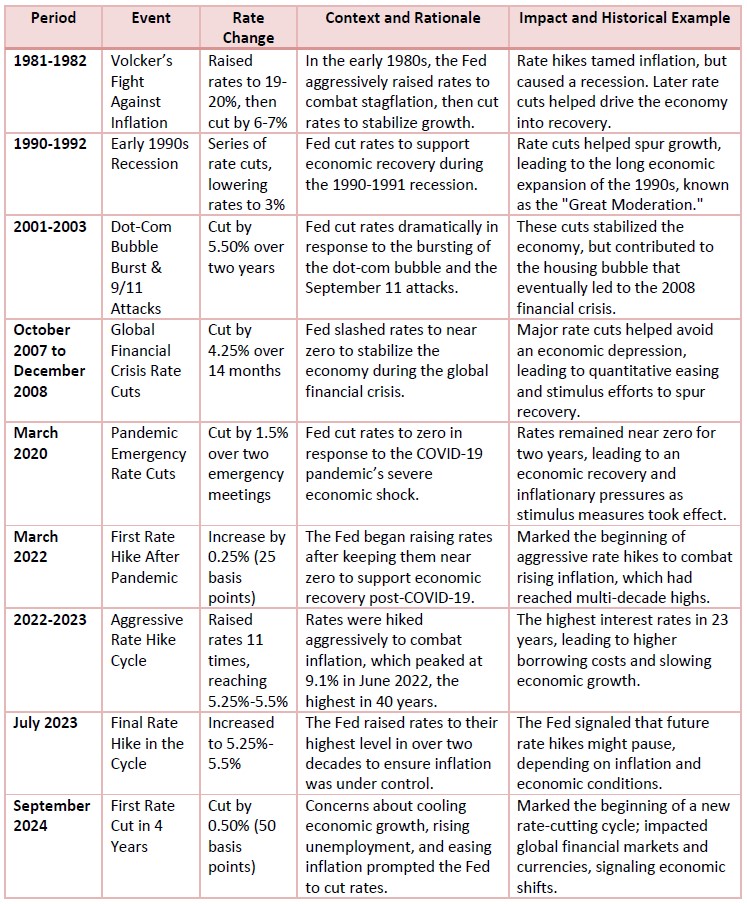

In 2024, for instance, the Federal Reserve implemented a 50-basis point cut, bringing the federal funds rate to a range of 4.75% to 5%.

This action followed more than a year of elevated interest rates, which had been raised aggressively from near-zero levels in response to inflation surging after the COVID-19 pandemic recovery.

The September 2024 rate cut was preemptive, aimed at bolstering a labor market showing early signs of cooling, and to prevent a potential recession.

Historical Context and Precedents

Historically, interest rate cuts have been employed during major economic crises.

In 2008, for example, the Fed slashed rates from 5.25% to near zero in response to the global financial crisis. Similarly, in early 2020, the onset of the COVID-19 pandemic led the Fed to cut rates to the 0%-0.25% range to provide immediate support to a collapsing global economy.

By comparison, the September 2024 cut followed a period where the federal funds rate had risen as high as 5.25%-5.50%, the highest level since the early 2000s.

This dramatic swing in interest rate policy underscores how rate cuts are often reactive measures, used after periods of tight monetary policy aimed at controlling inflation.

The aggressive rate hikes from 2022 to 2023 were designed to combat inflation, which peaked at 9.1% in mid-2022, the highest in over 40 years.

By cutting rates in 2024, the Fed aimed to ensure that inflation stayed under control while supporting economic growth as the labor market softened.

Risks and Potential Drawbacks of Interest Rate Cuts

While interest rate cuts stimulate growth, they can also introduce risks. One primary concern is the potential for inflation. If rates are cut too much, borrowing becomes too cheap, leading to an excessive influx of money into the economy.

This can result in demand outpacing supply, driving up prices and leading to inflationary pressures. For example, after the Fed slashed rates in 2020 to near zero, inflation skyrocketed in 2021 and 2022 as pent-up demand, supply chain issues, and labor shortages drove prices higher.

Low-interest rates make borrowing cheap, which can lead to speculation and inflated prices in assets such as real estate, stocks, or commodities.

For instance, in the early 2000s, low-interest rates contributed to the housing bubble that eventually led to the 2008 financial crisis.

In the current environment, concerns about inflated equity and real estate markets are prominent, especially with borrowing costs having been historically low for extended periods.

Furthermore, prolonged periods of low rates can distort financial markets.

Savers, for example, may find it difficult to earn meaningful returns on low-risk investments such as savings accounts or government bonds, pushing them into riskier assets in search of yield.

This risk-seeking behavior can lead to financial market instability, as was observed during the era of near-zero interest rates following the 2008 crisis.

Interest Rate Cuts as Economic Signals

Interest rate cuts also serve as powerful signals to financial markets and the public about the central bank’s view of the economy.

A rate cut often signals that the central bank is concerned about the trajectory of economic growth or inflation.

When the Fed cuts rates, it is generally seen as a sign that the economy is slowing or that the central bank is preemptively acting to stave off a downturn.

For instance, in 2024, while the U.S. economy was not yet in a recession, the Fed cut rates to mitigate risks arising from a cooling labor market and other economic vulnerabilities.

This preemptive action was meant to signal that the Fed would take steps to prevent a deeper slowdown.

On the flip side, unexpected or aggressive rate cuts can sometimes lead to market uncertainty, as investors may interpret them as a sign of looming economic trouble.

2. Timeline & Historical Analysis of Interest Rate Cuts

Interest rate cuts by the Federal Reserve are closely watched by economists, investors, and policymakers due to their profound impact on financial markets, borrowing costs, and overall economic activity.

To understand the significance of the Federal Reserve’s decisions, it is essential to explore the timeline and context of major rate cuts, especially in recent decades.

The 2020 Rate Cuts: Response to the COVID-19 Pandemic

The Federal Reserve’s most significant recent rate-cutting event occurred in March 2020, during the early days of the COVID-19 pandemic.

As the virus spread globally, triggering widespread economic shutdowns and financial market turmoil, the Fed moved swiftly to cut interest rates.

In a series of emergency actions, the federal funds rate was slashed from a range of 1.50%-1.75% down to 0%-0.25%.

This drastic reduction was an attempt to stave off a deep economic recession by providing cheap credit to businesses and households.

It was the first time since the 2008 financial crisis that rates had been brought down to near-zero levels.

The results of these rate cuts were immediate. Liquidity surged into financial markets, and borrowing costs for consumers and businesses fell sharply.

For instance, the average 30-year fixed mortgage rate dropped below 3%, spurring a housing boom as buyers sought to lock in historically low rates.

Stock markets, which had plunged in early 2020, rebounded strongly. The S&P 500 recovered from its March lows to reach new record highs by the end of the year.

The 2022-2023 Rate Hikes and the Return of Inflation

However, the recovery from the pandemic brought about new challenges.

The rapid injection of liquidity into the economy, coupled with supply chain disruptions, labor shortages, and rising consumer demand, led to a significant spike in inflation.

By mid-2021, inflation had reached levels not seen in decades, with the Consumer Price Index (CPI) climbing over 9% year-over-year in June 2022.

In response, the Federal Reserve shifted from an accommodative policy stance to a hawkish one, raising interest rates aggressively.

From March 2022 through July 2023, the Fed hiked interest rates 11 times, pushing the federal funds rate from near-zero to a range of 5.25%-5.5%, the highest level in more than two decades.

The purpose of these rate hikes was to cool the overheated economy and bring inflation back under control. While inflation did begin to decline toward the Fed’s 2% target—falling to around 3% by mid-2024—the hikes also began to weigh on economic growth, particularly in sectors sensitive to interest rates, such as housing and technology.

The September 2024 Rate Cut: A Pivotal Moment

After more than a year of holding rates at elevated levels, the Federal Reserve made a pivotal decision in September 2024 to cut interest rates by 50 basis points, bringing the federal funds rate to 4.75%-5%.

This marked the first rate cut in over four years and was widely anticipated by financial markets, which had been pricing in a potential easing of monetary policy due to signs of slowing economic growth and a softening labor market.

The September 2024 cut was described by the Fed as a preemptive move to support the labor market, which had been showing signs of cooling. Unemployment had ticked up slightly from its post-pandemic lows, and job growth had begun to slow.

Although inflation was no longer the immediate threat it had been in 2022, the Fed was concerned about the risk of a broader economic slowdown. By cutting rates, the Fed aimed to stimulate demand without stoking a new round of inflation.

This cut also signaled the beginning of a potential new rate-cutting cycle. With the economy entering a period of slower growth, many analysts predicted that the Fed could lower rates further in 2025, depending on the trajectory of inflation and employment.

Financial markets reacted positively to the cut, with major stock indices rising as investors anticipated that lower rates would boost corporate earnings and consumer spending.

Historical Context: Comparing Recent Cuts to Past Cycles

To fully understand the impact of the 2024 rate cut, it’s important to place it within the context of past rate-cutting cycles.

Since 1990, the Federal Reserve has undergone six major rate-cut and rate-hike cycles, each corresponding to different economic crises or recessions.

For example:

1990-1992: In response to a recession caused by rising oil prices and tighter monetary policy in the late 1980s, the Fed cut rates from 8% to 3% over a period of 18 months.

2001-2003: Following the burst of the dot-com bubble and the 9/11 terrorist attacks, the Fed slashed rates from 6.5% to 1% to stimulate a struggling economy.

2007-2009: During the global financial crisis, the Fed cut rates from 5.25% to near-zero, a period marked by massive economic contraction and financial instability.

Each of these rate-cutting cycles was followed by a period of recovery, though the speed and magnitude of the recovery varied based on the underlying causes of the economic downturn.

The 2024 rate cut is likely to be compared most closely to the rate cuts made in the aftermath of the 2001 recession and the 2008 financial crisis, as these events also followed aggressive periods of rate hikes.

Projections for Future Rate Cuts

Looking forward, many analysts expect that the Fed’s September 2024 cut could be the first in a series of reductions, depending on economic data in the coming months. Current forecasts suggest that the Fed could lower rates by an additional 100 to 150 basis points by the end of 2025 if inflation remains under control and growth continues to slow. However, the pace of these cuts will be highly dependent on the labor market and inflation data.

A key factor to watch will be whether the economy can avoid slipping into a recession. If the labor market weakens significantly or if inflation falls below the Fed’s 2% target, the central bank may opt for a more aggressive rate-cutting cycle. Conversely, if inflation begins to reaccelerate, the Fed could pause or slow the pace of cuts to avoid stoking new price pressures.

3. Impact on Various Asset Classes & Investment Opportunities

Interest rate cuts by the Federal Reserve have wide-reaching effects across all asset classes, from fixed income to equities, real estate, and commodities.

When the Fed lowers interest rates, the cost of borrowing declines, which directly and indirectly influences the returns on different investments.

Investors tend to shift their strategies in response to rate cuts, reallocating their portfolios to take advantage of lower borrowing costs and the potential for economic growth.

In this section, we will explore how interest rate cuts affect major asset classes, including bonds, equities, real estate, and currencies, supported by historical examples and current forecasts.

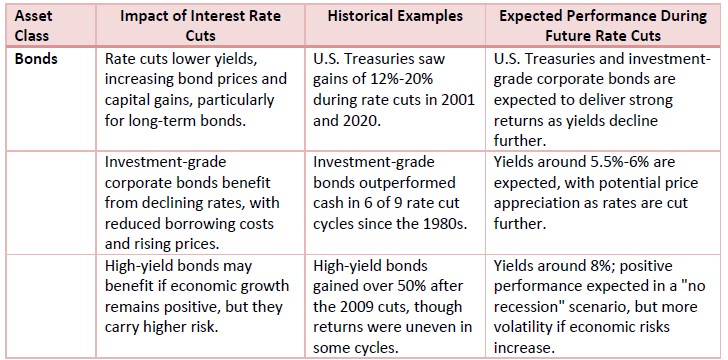

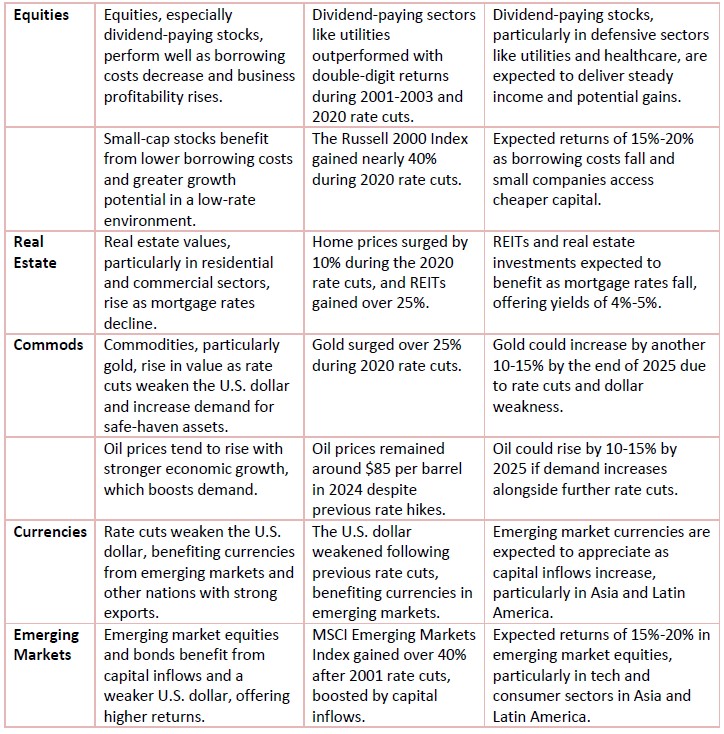

Bonds: The Primary Beneficiary

Fixed income assets, particularly government bonds, are usually the biggest beneficiaries of interest rate cuts.

Bond prices have an inverse relationship with interest rates—when rates fall, bond prices rise.

This is because new bonds issued after a rate cut offer lower yields, making existing bonds with higher coupon rates more attractive.

As demand for these higher-yielding bonds increases, their prices rise, providing capital gains to bondholders.

High-Yield Bonds

High-yield bonds, also known as “junk bonds,” can have a more mixed performance during rate-cut cycles.

These bonds, which are rated below investment grade (BB or lower), offer higher yields to compensate for their higher default risk.

In a “no recession” scenario, high-yield bonds often perform well as lower borrowing costs allow companies to refinance their debt more easily.

However, in the lead-up to or during a recession, high-yield bonds may underperform due to heightened credit risk.

For example, during the 2020 rate cuts, high-yield bonds experienced significant volatility.

While they rebounded strongly after the initial market panic subsided, many investors remained cautious due to concerns about rising default rates among riskier borrowers.

In 2024, high-yield bonds could see similar volatility, particularly if the U.S. economy enters a slowdown or mild recession.

However, if the Fed’s rate cuts successfully prevent a downturn, high-yield bonds could deliver strong returns, especially in sectors like energy and industrials.

Equities: Mixed Performance Depending on Economic Context

Stocks, or equities, typically benefit from lower interest rates, as cheaper borrowing costs support corporate profitability and boost economic activity.

However, the degree of impact varies depending on the broader economic context and the specific sector in question.

Growth Stocks vs. Value Stocks

Growth stocks, which are companies expected to grow at above-average rates, often benefit significantly from rate cuts.

These companies tend to rely more on external financing for expansion, and lower rates reduce the cost of this capital.

In past rate-cutting cycles, technology stocks have been major beneficiaries.

For instance, during the rate cuts following the 2008 financial crisis, the NASDAQ-100, heavily weighted toward tech companies, outperformed broader market indices, growing by over 50% in the first year of rate cuts.

In contrast, value stocks—companies trading below their intrinsic value, often with stable cash flows—may not benefit as much from rate cuts, although they still provide solid returns in certain environments. Value stocks in sectors like utilities and consumer staples tend to perform better in recessionary periods, as they are less sensitive to economic downturns and provide reliable dividends.

In 2024, with the Federal Reserve initiating a new cycle of rate cuts, growth stocks, particularly in sectors like technology and healthcare, are expected to outperform.

Companies such as Apple, Amazon, and Microsoft, which have large cash reserves and significant growth potential, stand to benefit from lower rates as their future cash flows are discounted at a lower rate, increasing their present value.

Value stocks, particularly in sectors like energy and financials, may lag behind but could still provide attractive dividend yields.

Small-Cap vs. Large-Cap Stocks

Small-cap stocks, which are companies with smaller market capitalizations, often benefit more from rate cuts than their larger counterparts.

These companies typically rely more heavily on short-term borrowing, so lower interest rates reduce their financing costs, boosting their bottom lines.

During the Fed’s last rate-cutting cycle in 2020, the Russell 2000, a small-cap index, outperformed the S&P 500, gaining nearly 40% by the end of the year.

In 2024, small-to-mid cap stocks are once again poised to outperform, particularly if the U.S. economy avoids a recession.

Analysts have noted that many small-cap companies are already seeing earnings acceleration, while large-cap companies are facing slowing profit growth.

As rate cuts reduce borrowing costs, small-cap companies in sectors like industrials and consumer discretionary could deliver significant returns, with some forecasts projecting gains of 15%-20% in 2025.

Real Estate: A Significant Beneficiary of Rate Cuts

Real estate, particularly through vehicles like real estate investment trusts (REITs), tends to benefit strongly from rate cuts.

Lower interest rates reduce mortgage costs for both commercial and residential real estate, making property more affordable and increasing demand.

This leads to rising property values and higher rental incomes for REITs.

In the 2020 rate-cutting cycle, real estate experienced a boom, with home prices soaring as mortgage rates dropped to historic lows.

The average 30-year fixed mortgage rate fell below 3%, spurring a wave of home buying and refinancing.

Similarly, commercial real estate saw a recovery as businesses took advantage of lower borrowing costs to expand or refinance existing debt.

In 2024, as rates begin to decline again, real estate markets are expected to benefit. REITs, which offer higher-than-average dividend yields, are particularly attractive to income-seeking investors.

The Vanguard Real Estate ETF (VNQ), a broad-based REIT index, could see significant inflows, with some analysts predicting returns of 10%-12% over the next 12 months as property values and rental incomes rise.

Currencies

When the Fed cuts interest rates, the U.S. dollar tends to weaken relative to other major currencies, as lower rates reduce the yield on dollar-denominated assets, making them less attractive to foreign investors. In 2024, following the September rate cut, the U.S. dollar index (DXY) fell by around 1%, and further cuts are expected to push the dollar down by an additional 3%-5% in 2025.

A weaker dollar benefits U.S. exporters by making American goods cheaper abroad, which could boost sectors like manufacturing and agriculture.

Commodities

Commodities such as gold and oil often react differently to rate cuts.

Gold, traditionally seen as a hedge against inflation and currency depreciation, tends to rise when interest rates fall, as the opportunity cost of holding non-yielding assets decreases.

In 2020, gold prices surged by over 25% as rates dropped to near zero.

In 2024, with further rate cuts on the horizon, gold is expected to perform well, with some analysts forecasting prices to reach $2,200 per ounce by mid-2025.

Oil prices, on the other hand, are more sensitive to global economic growth.

While lower rates can boost demand by stimulating economic activity, oil markets are also affected by supply dynamics and geopolitical events.

In 2024, oil prices remained relatively stable following the Fed’s rate cut, hovering around $85 per barrel.

However, if rate cuts successfully stimulate growth in emerging markets, demand for oil could increase, pushing prices higher in 2025.

4. Conclusion

Interest rate cuts represent one of the most powerful tools that central banks, such as the Federal Reserve, have at their disposal to influence economic conditions.

These cuts lower the federal funds rate, making borrowing cheaper for businesses and consumers.

The main objective is to stimulate economic activity by encouraging spending and investment, particularly during times of economic slowdown or financial distress.

The Fed’s recent 50-basis point cut in September 2024, the first in over four years, marks a pivotal shift in its monetary policy after an extended period of aggressive rate hikes to combat inflation.

Historically, rate cuts aim to stabilize inflation, support the labor market, and mitigate the risks of a recession, but the effectiveness of these cuts depends heavily on the broader economic context and timing.

The timeline of rate cuts and hikes reveals that these shifts often come in response to economic crises.

Since 1990, six major rate-cut cycles have occurred, often following periods of financial stress, such as the dot-com bubble, the 2008 global financial crisis, and the COVID-19 pandemic.

The 2024 cuts, coming after an aggressive hiking cycle that pushed rates to a 23-year high, signal the Fed’s concerns over cooling economic growth and rising unemployment.

These cuts are expected to continue into 2025, potentially providing significant relief to global economies, particularly those with dollar-denominated debt.

The impact of interest rate cuts spans multiple asset classes, with bonds typically being the primary beneficiaries. U.S. Treasuries, investment-grade corporate bonds, and high-yield bonds all perform well when rates fall, as the cost of borrowing decreases, leading to capital gains.

Equities, particularly dividend-paying stocks and small-cap companies, also tend to benefit from rate cuts, as lower interest rates support higher corporate earnings and growth potential.

Real estate, both residential and commercial, sees increased demand due to lower mortgage rates, making real estate investment trusts (REITs) a key area of opportunity for income-seeking investors.

Commodities like gold often rise as rate cuts weaken the U.S. dollar, while oil prices can increase with stronger economic demand.

Looking ahead, the current rate-cut cycle presents a range of potential investment opportunities.

Bonds, especially U.S. Treasuries and investment-grade corporate bonds, are poised for capital gains as yields decline.

Dividend-paying stocks and small-cap equities may outperform, driven by lower financing costs and improved earnings. Real estate remains a significant beneficiary, with REITs offering attractive yields in a low-rate environment.

Commodities, particularly gold and oil, could experience price appreciation, while emerging markets stand to gain from increased capital inflows and a weaker dollar.

Investors should consider these opportunities and adjust their portfolios accordingly as the Fed continues its rate-cutting policy into 2025.

As we come to the end of the report, here are some questions to ponder about:

1. With interest rates expected to decline further, how can investors balance the risks of inflation with the potential for growth in fixed-income assets like bonds?

2. As emerging markets stand to benefit from a weaker U.S. dollar and lower rates, what are the potential geopolitical risks that could influence their long-term growth prospects?

3. Given that rate cuts can stimulate both positive economic growth and excessive risk-taking, how can central banks effectively manage the delicate balance between fostering growth and preventing asset bubbles in financial markets?

The Little Book of Common Sense Investing (Bogle): Summary and Key Ideas

Last updated: 3 July 2026 · By Spencer Li, CFTe

“The Little Book of Common Sense Investing” by John C. Bogle argues that the surest way for an ordinary investor to build wealth is to buy a low-cost index fund (a fund that simply tracks the whole market instead of trying to beat it), hold it for decades, and stop trying to be clever. Bogle, who founded Vanguard and created the first index fund for everyday investors, makes one core case across the whole book: most investors, professionals included, cannot beat the market consistently, and the fees they pay trying to do so quietly eat their returns. So the rational move is to own the market cheaply and let compounding do the work. The book is short, plain, and almost boring on purpose. That is the point. It is a manual for getting out of your own way.

I read this as a trader, not as a passive investor, and I still think it is one of the most important investing books ever written. Here is why, what is actually in it, and how a trader should read it.

Who is John Bogle, and why listen to him?

John C. Bogle (1929 to 2019) founded the Vanguard Group in 1975 and launched the first index mutual fund available to the public the following year. At the time, the idea of a fund that deliberately did not try to outperform was treated as a joke. Today index funds hold trillions of dollars, and Bogle is often called the “godfather of index funds.”

What makes him credible is that he spent a career arguing against his own industry’s profit centre. Fund companies make money from fees. Bogle’s whole message was that those fees are the enemy of the investor. He built Vanguard as a client-owned structure so it could keep costs low. Hence the no-nonsense tone of the book: he is not selling you a product. He is telling you to buy the cheapest, dullest thing on the shelf.

What is the book actually about?

The book makes one argument and defends it from several angles: own the entire market through a low-cost index fund, hold for the long term, and refuse to be talked out of it.

Bogle’s reasoning runs like this. The stock market, over a long enough horizon, delivers a return that reflects the real growth of the businesses inside it. That return is there for the taking. The problem is that investors keep subtracting from it: trading costs, management fees, taxes from churn, and bad timing decisions driven by fear and greed. An index fund minimises every one of those leaks. You capture close to the full market return because you are not paying anyone to try (and usually fail) to beat it.

The villain of the book is cost. Bogle’s most quotable idea is simple: in investing, you get what you don’t pay for. A 2% annual fee sounds small. Over 30 years of compounding, it can quietly consume a large slice of your final wealth. That is the engine behind everything else he says.

The core ideas, without the repetition

The source material for this book lists the same handful of points many times over. Stripped down, Bogle is really making six arguments:

Own the whole market. A broad index fund gives you instant diversification (spreading money across many holdings so no single one can sink you) at almost no cost.

You probably can’t beat the market, and neither can the pros. The majority of actively managed funds underperform their index over the long run, especially after fees.

Cost is the thing you can actually control. You cannot control returns. You can control how much you pay, so drive it to the floor.

Compounding rewards time, not cleverness. Start early, stay invested, and let the math run. Trying to get rich quickly usually does the opposite.

Your emotions are the other enemy. Fear and greed make people sell at bottoms and buy at tops. A simple plan you can hold through a crash beats a brilliant plan you abandon in a panic.

Simplicity wins. The more moving parts, the more places to leak money and nerve. Boring is a feature.

Active funds vs index funds, over time

Here is the comparison at the heart of Bogle’s case, laid out plainly:

Active fund

Low-cost index fund

Goal

Beat the market

Match the market

Typical cost

High (management fees, trading, taxes from churn)

Very low

Long-run record vs index

Most underperform after fees

Tracks the market by design

What you rely on

A manager’s skill staying hot for decades

The market’s long-term growth

Effort to run

Picking and switching funds

Buy, hold, ignore

Bogle’s verdict

A bet against the odds

The rational default

Do note that this is the long-horizon picture. Over a single year, plenty of active funds beat the index. The trouble is that the winners rarely repeat, and you cannot know in advance which ones they will be. Across decades, the cost drag compounds and the odds tilt hard toward the cheap, simple option.

How should a trader read this book?

This is the part people get wrong. They see “index funds win” and assume Bogle is telling everyone to never trade. That is not the lesson I take.

Personally, I run two separate buckets, and this book governs only one of them. The long-term bucket is exactly what Bogle describes: low-cost, diversified, automatic, untouched. It is the foundation. The active bucket is where I trade with a defined system, defined risk, and a public log. The mistake is mixing the two, treating your serious savings like a casino, or treating your trading capital like it should be left alone for 30 years.

So read Bogle as the floor, not the ceiling. He is right that most people who try to beat the market lose to it. He is also describing exactly why a disciplined, low-cost, rules-based approach matters whether you are indexing or trading. The discipline is the same. Cut costs, control emotions, think in decades, and do not confuse activity with progress.

Here is the one honest caveat. If you are going to trade actively, Bogle’s data is a warning shot, not an insult. It tells you the bar is high and the average participant is below it. That should make you more rigorous about edge, sizing, and process, not less. A fund manager with a research team usually fails to beat a dumb index. That is the company you are choosing to keep when you decide to trade, so bring a real system or don’t bother.

Where the human edge comes in

An index fund is the ultimate “let the machine do it” investment. You hand the whole job to a rules-based vehicle and walk away, and for most people that is the right call. The judgment is not in running it. It is in deciding which money belongs there and which money you are willing to actively manage, sizing each bucket to your real life, and then having the discipline to leave the long-term bucket alone through a 30% drawdown. The fund captures the market return. Whether you actually keep it is down to your behaviour, and that is the first of the Five Edges no fund can supply for you.

FAQ

What is the main message of The Little Book of Common Sense Investing?

Buy a low-cost index fund that owns the whole market, hold it for the long term, and stop trying to beat the market. Bogle argues that low cost and simplicity, not stock-picking skill, are what actually drive long-term investing success.

Is The Little Book of Common Sense Investing worth reading?

Yes, especially if you are new to investing or want to simplify a portfolio that has drifted into too many funds and fees. It is short, plain, and built around one durable idea. Experienced traders also benefit from it as a reminder of how much cost and emotion quietly cost you.

What does Bogle mean by “you get what you don’t pay for”?

He means that in investing, lower cost directly raises your net return. Because you cannot control the market’s return, the fees you avoid are the most reliable way to keep more of what the market gives. Over decades of compounding, even a small annual fee can consume a large share of your final wealth.

Does Bogle say you should never trade or pick stocks?

He argues that most investors, including professionals, fail to beat the market consistently, so for the bulk of your money, indexing is the rational default. He does not claim it is impossible to trade well, only that the odds are against the average participant, which is a reason to be disciplined rather than reckless.

Are index funds really safer than active funds?

Index funds are not immune to market crashes, since they fall with the market they track. What they remove is the extra risk of a single manager underperforming and the steady drag of high fees. Bogle’s point is about reliability and cost, not about avoiding market risk altogether.

Now that you have Bogle’s case for the boring, low-cost, long-term approach, the real question is which of your money it should govern, and which money you are willing to actively trade with a real system. Have you read this one? Let me know your key takeaway in the comments.

Want a system for the active side of the ledger? Grab the free 15-Minute Swing Trading Starter Kit, the exact routine I use to scan once a day and trade any market in 15 minutes.

About the author. Spencer Li is the founder of Synapse Trading and a Certified Financial Technician (CFTe) with 15 years of trading across stocks, forex, crypto, commodities, and bonds. His trade log is public, 404 trades, losses left in. He teaches low-risk swing trading in 15 minutes a day, one system for any market.

Education, not financial advice. Synapse Trading is not licensed by MAS to advise on investment products. Trading carries risk of loss; past performance is not indicative of future results.

https://synapsetrading.com/wp-content/uploads/2023/01/thumbnail-Book-Summary-The-Little-Book-of-Common-Sense-Investing.png7201280Spencer Lihttps://synapsetrading.com/wp-content/uploads/2019/10/logo.jpgSpencer Li2024-08-05 19:30:072026-07-03 16:37:47Book Summary: The Little Book of Common Sense Investing by John C. Bogle

The yen carry trade has long been a cornerstone of global financial strategies, allowing investors to leverage Japan’s low-interest rates for higher returns abroad.

However, recent developments have put this once-reliable trade under pressure.

In this blog post, I will explain what the yen carry trade is, its historical context, the reasons behind its current unwinding, and how it will affect the various financial markets.

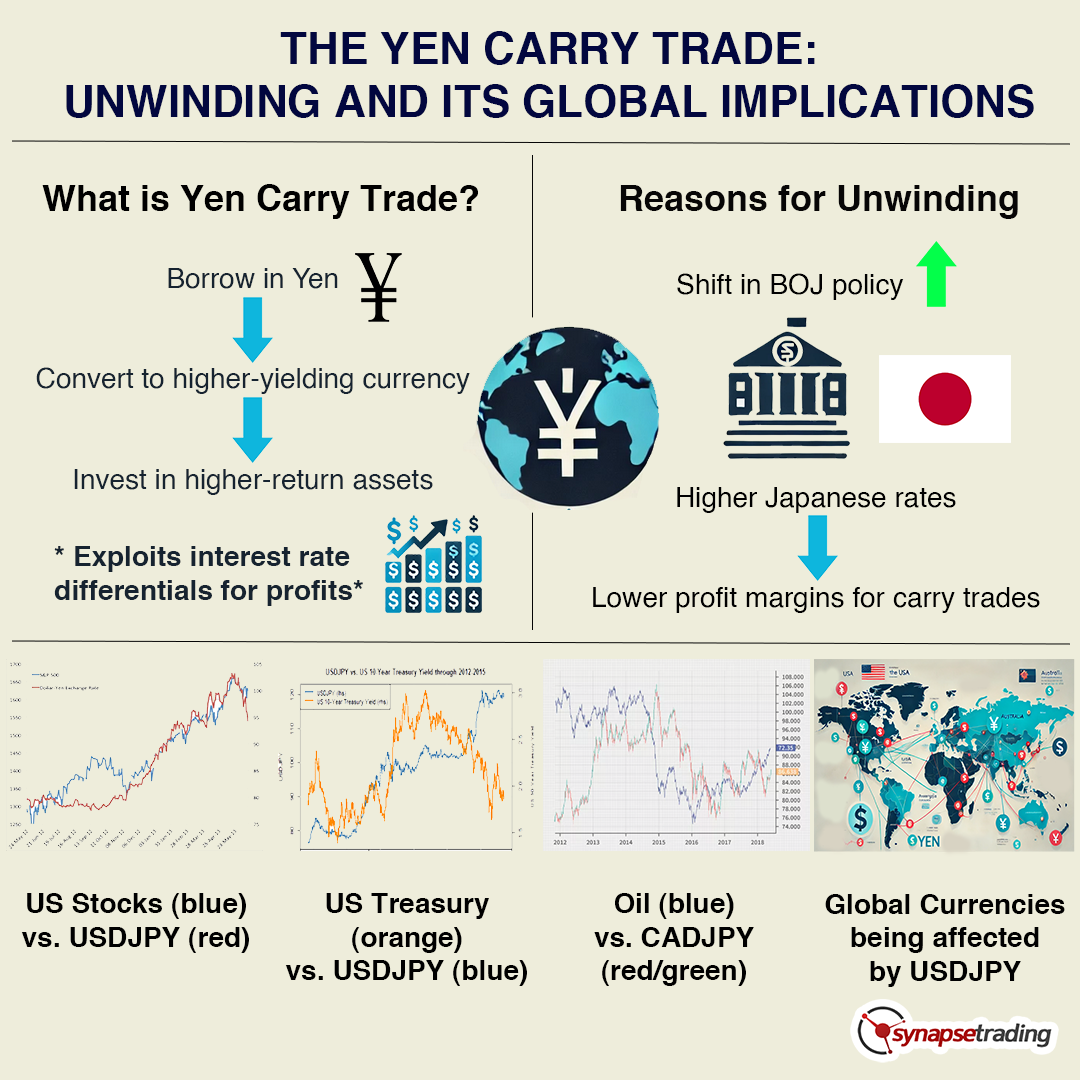

What is the Yen Carry Trade?

The yen carry trade involves borrowing funds in Japanese yen, where interest rates are typically very low, and then converting these funds into a currency with higher interest rates to invest in assets that yield better returns.

This strategy exploits the differential in interest rates between Japan and other countries, allowing investors to profit from the spread. Historically, it has been a lucrative endeavor, with minimal cost for borrowing in yen and potential for significant gains in higher-yielding currencies and assets.

To elaborate, the core mechanism of the yen carry trade is based on the interest rate differential. Japan has maintained one of the lowest interest rates among developed countries, often near or at zero.

Investors borrow in yen at these low rates and convert the yen into currencies like the U.S. dollar or Australian dollar, where interest rates are higher. The borrowed funds are then invested in assets that provide higher returns, such as government bonds, corporate bonds, equities, or real estate in those higher-yielding currencies.

The profit for the investor comes from the difference between the low cost of borrowing in yen and the higher returns on the investments made in other currencies.

For example, if an investor borrows yen at an interest rate of 0.1% and invests in U.S. Treasury bonds yielding 2%, the investor earns the difference, minus any exchange rate changes. This trade is particularly attractive during periods of stable or appreciating currencies against the yen, as any gain in the target currency further enhances returns.

Historical Context

The yen carry trade gained popularity in the late 1990s and early 2000s as Japan maintained ultra-low interest rates in response to its prolonged economic stagnation. The Bank of Japan’s (BOJ) commitment to near-zero rates created a fertile ground for this strategy.

Investors flocked to borrow in yen and invest in higher-yielding assets worldwide, driving significant capital flows across global markets. This trade contributed to liquidity in financial markets and often amplified asset price movements.

In the 1990s, Japan’s economy was grappling with the aftermath of the asset bubble burst. The BOJ slashed interest rates to stimulate economic activity, making borrowing extremely cheap.

This environment catalyzed the yen carry trade, attracting global investors who could borrow yen at negligible costs. By the early 2000s, this strategy was widespread, influencing capital flows and asset prices globally.

The 2008 financial crisis marked a significant moment for the carry trade. As global markets plunged, investors scrambled to unwind their yen positions, leading to a sharp appreciation of the yen.

This episode highlighted the inherent risks of the carry trade—while it could be highly profitable in stable times, it also posed substantial risks during periods of market turbulence.

Why is the Trade Unwinding Now?

The yen carry trade is unwinding primarily due to the recent policy shifts by the Bank of Japan. For the first time in many years, the BOJ has signaled an end to its ultra-loose monetary policy by lifting its main interest rate. This move, aimed at combating inflation and stabilizing the economy, has had profound implications for the carry trade.

As Japan’s interest rates rise, the cost of borrowing in yen increases, reducing the profitability of the carry trade. Consequently, investors are beginning to unwind their positions, repaying yen-denominated debt and selling off foreign assets.

In detail, the BOJ’s decision to raise interest rates is a response to rising inflationary pressures. Japan, historically plagued by deflation, is now facing inflationary trends similar to other advanced economies.

To curb inflation, the BOJ has started to tighten its monetary policy, which includes raising interest rates. This change increases the cost of borrowing in yen, thereby diminishing the appeal of the carry trade.

As the yen appreciates, the cost of repaying yen-denominated loans increases, prompting investors to close their positions.

The rapid unwinding has created significant volatility in financial markets, particularly in assets that were popular targets of the carry trade, such as U.S. equities and emerging market currencies.

What is the Significance of This?

The unwinding of the yen carry trade is significant for several reasons.

Firstly, it signals a major shift in Japanese monetary policy, which has been a cornerstone of global financial markets for decades.

Secondly, it highlights the interconnectedness of global markets, where a policy change in Japan can ripple through to impact asset prices and capital flows worldwide. The yen exchange rate has become a key driver of global markets, indicating the profound influence of Japanese monetary policy on international financial dynamics.

This shift underscores the global dependency on Japanese monetary policy.

For years, the yen carry trade has been a source of global liquidity, supporting asset prices and economic growth in various regions. The BOJ’s policy shift not only affects Japan but also has broad implications for global financial stability.

The yen’s appreciation and the subsequent market reactions demonstrate how deeply intertwined global financial systems are, with Japan playing a pivotal role.

How Does it Affect the Markets?

The impact of the yen carry trade unwinding is already being felt across various markets.

The rapid appreciation of the yen against the U.S. dollar has caught many market participants off guard. Over the last month, the yen has surged approximately 8% against the dollar, a stark contrast from its depreciation earlier in the year. This sudden rally has triggered a sell-off in U.S. equities, as investors unwind their carry trade positions, leading to downward pressure on asset prices.

This market reaction highlights the vulnerabilities in financial markets to changes in the yen exchange rate. The appreciation of the yen increases the cost of repaying yen-denominated debt, prompting investors to liquidate assets to meet these obligations. This selling pressure has led to declines in equity prices and increased volatility in financial markets.

Deep Dive on Specific Markets

U.S. Equities: The U.S. stock market has experienced increased volatility and a broad slump as the yen appreciates. The unwinding of the carry trade leads to selling pressure on U.S. equities, exacerbating declines in stock prices. This negative reaction of U.S. equity prices is an early warning of the challenges ahead.The relationship between the yen carry trade and U.S. equities is significant because many investors use borrowed yen to invest in U.S. stocks. When the yen strengthens, these investors face higher costs to repay their loans, leading them to sell their U.S. stock holdings. This selling pressure contributes to market declines and increased volatility.

U.S. Government Debt: The yields on U.S. government bonds have also been affected. As investors sell foreign assets to repay yen-denominated debt, there is a shift in demand dynamics for U.S. Treasuries, influencing yields and bond prices.Typically, during periods of financial stress, U.S. Treasuries are seen as a safe haven. However, the unwinding of the carry trade can lead to complex dynamics. While some investors may flock to Treasuries for safety, others may sell them to cover their yen-denominated liabilities, leading to fluctuating yields.

Global Currency Markets: The yen’s rally has had a ripple effect on other currencies, particularly those that were heavily borrowed against in carry trades. This includes higher-yielding currencies like the Australian dollar and emerging market currencies, which have seen increased volatility and depreciation against the yen.The strength of the yen affects global currency markets by altering the dynamics of capital flows. Currencies that were favored in carry trades may experience significant depreciation as investors unwind their positions. This can lead to heightened volatility and potential financial instability in countries reliant on these capital flows.

Commodities: Commodity markets are also impacted as the unwinding of the carry trade affects global liquidity and risk sentiment. A stronger yen can lead to reduced commodity prices, as Japan is a significant importer of raw materials.Commodities are sensitive to changes in global liquidity and risk sentiment.The unwinding of the carry trade can reduce liquidity, leading to lower demand for commodities. Additionally, a stronger yen makes imports cheaper for Japan, potentially reducing the global prices of commodities such as oil and metals.

Concluding Thoughts

The unwinding of the yen carry trade is a pivotal development in global financial markets, driven by the Bank of Japan’s shift in monetary policy. Its effects are far-reaching, impacting equities, bonds, currencies, and commodities worldwide. As the yen appreciates, the vulnerabilities in global markets are laid bare, underscoring the interconnectedness of financial systems.

Investors and policymakers alike must navigate these changes with an understanding of the intricate dynamics at play, ensuring strategies are adapted to this new financial landscape.

Now that I have shared all about the Yen carry trade unwinding, here are some questions to ponder about:

How might the unwinding of the yen carry trade influence the stability and valuation of emerging market currencies that were previously beneficiaries of this strategy?

What potential long-term impacts could the shift in Japanese monetary policy have on global equity markets, particularly in terms of investment flows and asset allocation strategies?

https://synapsetrading.com/wp-content/uploads/2024/08/blog-post-thumbnail-yen-carry-trade.png10241792Spencer Lihttps://synapsetrading.com/wp-content/uploads/2019/10/logo.jpgSpencer Li2024-08-05 14:39:392024-08-08 15:23:11The Yen Carry Trade: Unwinding and Its Global Implications

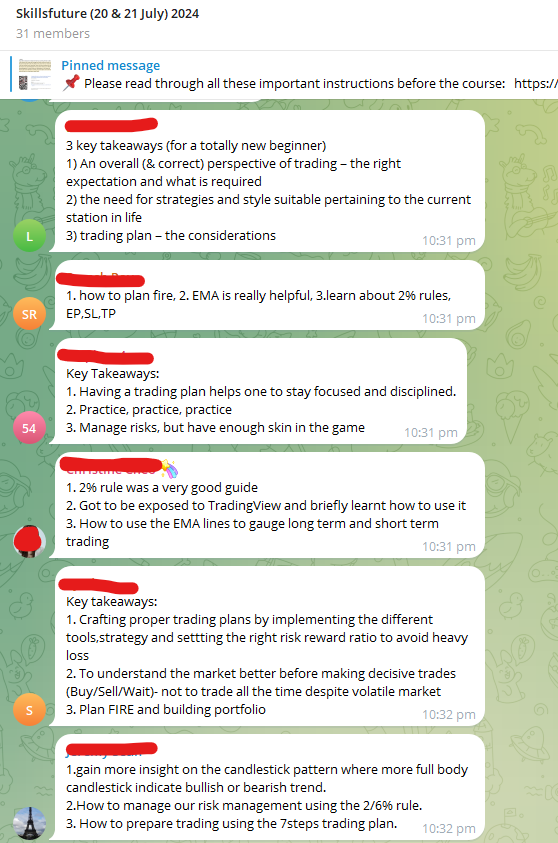

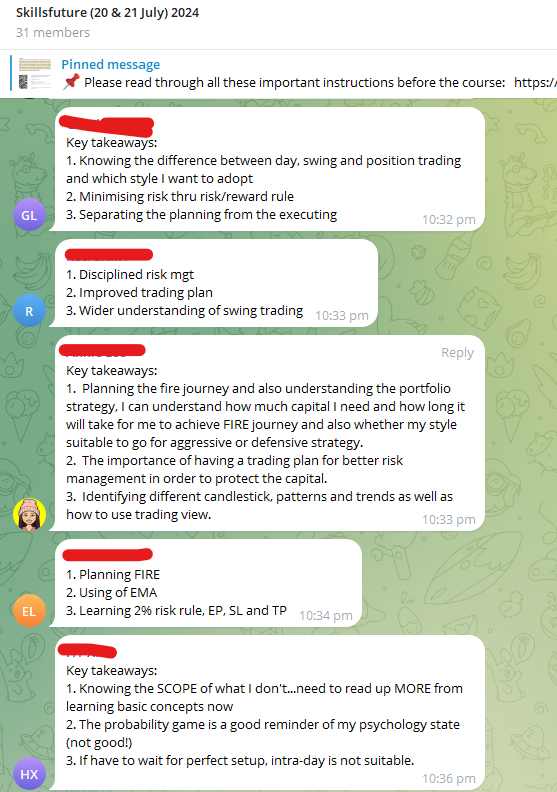

Last week, we conducted another online workshop on the basics of trading and investing, and since it is a SkillsFuture Credit-Eligible Course, participants could use their SkillsFuture credits to pay for the course instead of cash.

Thanks for the support!

During the 9 hours of training, participants learnt portfolio strategies to build and protect their wealth, as well as trading skills like market-timing, chart-reading and risk management to improve their trading results.

Here is some of the feedback and learning points from participants, after our hands-on market analysis session to find trading opportunities in the market.

If you are keen to learn more using your SkillsFuture credits, click this link to check availablity: