The U.S. presidential election results for 2024 are in, and Donald Trump has won his second term. The Republicans not only secured the White House but also gained control of the Senate, and potentially the House of Representatives, though this is yet to be confirmed.

This powerful combination places Trump in one of the strongest positions a U.S. president has held in modern history, giving him significant latitude to pursue his agenda without as many checks from Congress, at least until the 2026 midterm elections.

This outcome has far-reaching implications for investors in 2025, given the policies Trump is likely to pursue, from aggressive fiscal spending to potential tariffs on international trade partners.

In this post, we will explore how various asset classes performed during Trump’s first presidency, examine key changes in the economic landscape, and provide insights on the best assets to hold in the current environment.

How Did Various Asset Classes Fare During Trump’s Last Presidency?

Under Trump’s first term (2017-2021), financial markets were largely favorable to equities, especially those in sectors directly impacted by his policies. Here’s a quick look at how key asset classes and sectors performed:

- Equities: Stock markets surged, with the Dow Jones Industrial Average gaining 56% over Trump’s term, an impressive annualized return of around 11.8%. Corporate tax cuts were a significant factor, boosting the profitability of many companies. Technology, financial, and defense stocks performed particularly well, as they benefited from both tax incentives and a reduction in regulatory burdens.

- Energy Sector: Despite policy support for fossil fuels, the energy sector saw mixed results due to global oil price volatility and competition from renewable energy. Nevertheless, Trump’s pro-oil policies did offer some support to traditional energy players like ExxonMobil (XOM) and Chevron (CVX).

- Real Estate: Real estate assets saw positive gains during Trump’s first term, especially as interest rates remained relatively low, fostering demand for property investments.

- Gold and Commodities: Gold benefited as a safe-haven asset, especially during periods of geopolitical tension. Other commodities also showed resilience, especially those with inelastic demand.

- Cryptocurrencies: Cryptocurrencies gained traction as decentralized assets, independent of government intervention. Bitcoin, in particular, hit new highs toward the end of Trump’s term, and it continues to attract attention as a potential hedge against inflation and economic uncertainty.

What’s Different This Time?

While Trump’s new term brings some policy continuity, the macroeconomic landscape in 2025 is very different from 2017. Here are some major changes:

- Post-Pandemic Recovery: The global economy is still adjusting from the aftereffects of the COVID-19 pandemic. Supply chain challenges, labor shortages, and rising production costs have reshaped economic dynamics, influencing inflation and wage levels.

- Elevated National Debt: The U.S. debt has continued to grow, posing additional challenges for fiscal policy. Trump’s potential push for tax cuts and increased fiscal spending may lead to more borrowing, which could heighten the risk of inflationary pressures and increase long-term interest rates.

- Geopolitical Tensions: Tensions with China persist, and the ongoing conflict between Russia and Ukraine has added complexity to global trade and energy markets. Trump’s policies could reignite trade conflicts, though he may seek to negotiate deals to benefit U.S. interests.

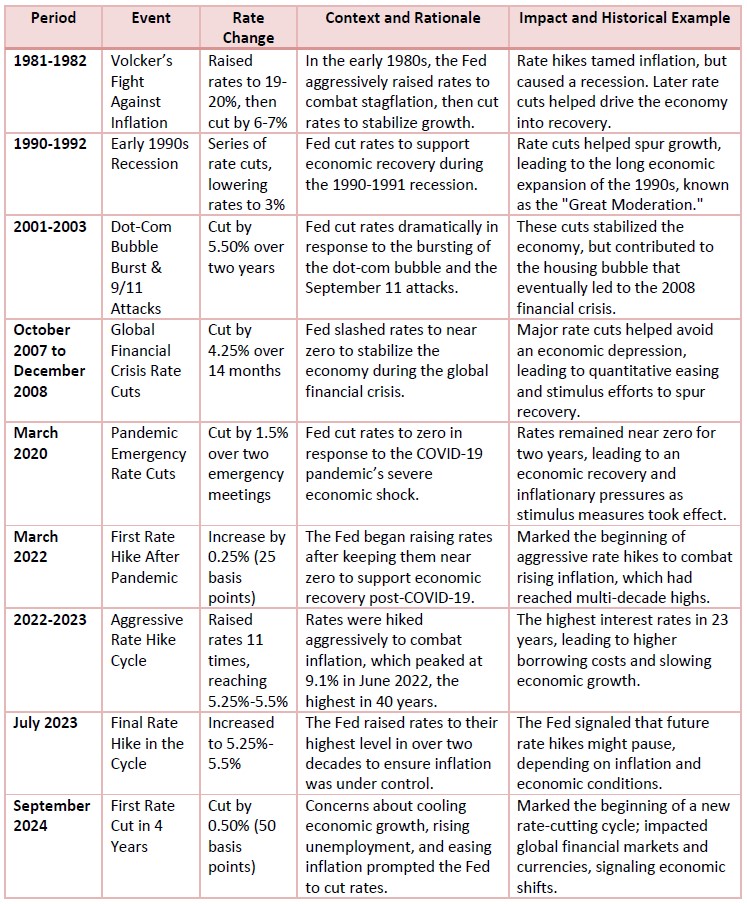

- Federal Reserve Policy: The Federal Reserve has already started cutting interest rates, with more reductions projected over the next few months. This accommodative stance aims to stimulate economic growth but may fuel inflationary pressures, especially if paired with fiscal expansion.

Will Inflation Return in 2025?

Inflation is a key concern heading into 2025, and Trump’s policies could amplify it. His America-first approach often includes:

- Large Fiscal Spending: Infrastructure projects and defense spending could drive up government expenditures.

- Lower Taxes: Reduced taxes can increase disposable income, but they also expand the federal deficit.

- Potential Tariffs: Trade tariffs may raise prices on imported goods, adding to inflationary pressures.

The Fed’s recent rate cuts, aimed at stimulating the economy, could further heighten inflationary risks if demand outpaces supply. Although inflation has eased recently, these combined factors make a resurgence in 2025 likely.

One scenario is that the Fed may allow nominal GDP to grow faster than inflation, helping to reduce the real burden of national debt. However, this approach risks a “Liz Truss moment” if investors lose confidence in the U.S.’s fiscal management, causing bond yields to spike and leading to market instability.

Will There Be a Recession or Market Crash?

The question of a potential recession or market crash depends on the balance between economic growth and inflation control.

Trump’s pro-growth policies, such as tax cuts and deregulation, could stimulate economic expansion.

However, unchecked spending and low interest rates might lead to overheating, which could result in a subsequent downturn.

If the Fed is forced to raise interest rates abruptly in response to rising inflation, the risk of a recession or market crash increases.

Similarly, geopolitical instability or an unforeseen financial crisis could trigger volatility.

Investors should be cautious of high debt levels and be prepared for potential shocks to the system.

Best Assets to Invest in Under President Trump’s New Term

With the potential for inflationary pressures, fiscal stimulus, and geopolitical shifts, the following assets and sectors could present valuable opportunities for investors. Here’s a deeper look at each category:

a) Hard Assets (Gold, Commodities, Real Estate)

Gold and Commodities:

Gold has historically served as a hedge against inflation and currency devaluation, making it an appealing choice in a Trump administration likely to encourage inflationary spending. Trump’s fiscal policies—especially increased government spending on infrastructure, defense, and subsidies—could stimulate inflation, which would enhance gold’s value as a safe-haven asset.

Commodities, including oil, natural gas, and agricultural products, are also likely to benefit. These hard assets have intrinsic value and limited supply, making them resilient in inflationary climates. For example, with potential tariffs on imported goods and raw materials, domestic agricultural and industrial commodities could experience price gains due to limited supply chains.

Real Estate:

Real estate can offer stability in an inflationary environment, as property values and rental income generally rise with inflation. Investors in prime real estate may benefit from demand-driven rental increases. However, for those investing in Real Estate Investment Trusts (REITs), it’s essential to be mindful of volatility driven by interest rate fluctuations. REIT prices tend to decline when long-term interest rates rise, as higher yields on bonds and other fixed-income investments become more attractive in comparison.

b) Cryptocurrencies (Bitcoin, Ethereum)

Bitcoin and Ethereum:

Cryptocurrencies like Bitcoin and Ethereum are increasingly regarded as “digital gold” due to their decentralized nature and scarcity. In an era where fiscal expansion and debt accumulation might undermine traditional fiat currencies, Bitcoin, in particular, stands out as an alternative store of value. Investors may flock to Bitcoin and other cryptocurrencies as hedges against inflation, seeking assets uncorrelated to traditional financial markets.

Crypto Mining Companies:

With the potential rise in demand for digital assets, crypto mining companies, such as Marathon Digital (MARA) and Riot Platforms (RIOT), are well-positioned to benefit. These companies mine Bitcoin and other cryptocurrencies, and they often see their stock prices rise alongside cryptocurrency prices. Increased regulatory support or at least a hands-off approach to the crypto sector from the Trump administration could further drive growth for these companies.

c) Conventional Energy (Oil and Gas Stocks)

Oil and Gas Companies:

Trump’s administration has historically supported traditional energy industries, often rolling back environmental regulations and promoting fossil fuel production. This favorable policy environment could benefit companies like ExxonMobil (XOM), Chevron (CVX), and Occidental Petroleum (OXY), which could see profitability increases if oil prices rise due to heightened demand and reduced regulatory costs.

However, investors should keep an eye on the global shift toward renewable energy. The growth of green energy and global commitments to reduce carbon emissions could temper the growth potential for oil and gas companies in the longer term. While Trump’s policies may provide a short-term boost, a diversified approach within the energy sector—including a mix of conventional and renewable energy investments—could offer a more balanced risk profile.

d) Financials

Banks and Financial Institutions:

Banks such as JPMorgan Chase (JPM), Bank of America (BAC), and Wells Fargo (WFC) could benefit from Trump’s potential deregulation initiatives. Deregulation could reduce compliance costs, streamline operations, and allow banks to take on more leverage, potentially increasing profitability. Additionally, Trump’s policies may stimulate economic activity, which could lead to higher demand for loans, further boosting bank earnings.

Moreover, if inflation rises, the Federal Reserve may eventually raise interest rates, benefiting banks by widening their net interest margins (the difference between the interest banks earn on loans and the interest they pay on deposits). This would be especially favorable for large banks with extensive lending operations.

e) Industrials and Defense Stocks

Infrastructure and Defense Companies:

Industrials, especially companies involved in infrastructure, may see increased opportunities. Trump has shown a strong preference for infrastructure spending, which may drive demand for companies like Caterpillar (CAT) that provide construction machinery and equipment. Infrastructure development would likely receive a fiscal boost, creating growth prospects for industrial firms that support public works, transportation, and urban development projects.

Defense Contractors:

Defense spending may also increase under Trump’s administration, benefiting companies such as Lockheed Martin, Northrop Grumman, and General Dynamics. Trump’s commitment to a strong national defense and bolstered military spending could create a favorable environment for these firms, which manufacture advanced defense technologies and equipment for the U.S. government and its allies.

f) Technology Stocks

Large-Cap Technology Companies:

Despite Trump’s previous criticisms of certain tech giants, the technology sector remains a cornerstone of the U.S. economy and a key driver of innovation and growth. Companies with strong pricing power, established market positions, and diversified revenue streams—such as Apple (AAPL), Microsoft (MSFT), and Alphabet (GOOGL)—are better positioned to withstand inflationary pressures.

The sector may face some challenges if Trump imposes new tariffs on tech components imported from China. This could raise costs for companies heavily dependent on international supply chains. However, companies with the ability to innovate, shift production, or pass costs to consumers are likely to fare well.

High-Growth and Emerging Tech:

Additionally, emerging sectors like artificial intelligence (AI), cybersecurity, and cloud computing could continue to thrive, driven by growing demand for digital transformation and data protection. Investors seeking exposure to long-term growth should consider companies in these high-potential segments of the technology market.

g) Agricultural Stocks

Agricultural and Farming Companies:

Agriculture is a key sector in Trump’s “America First” agenda, and companies like Deere & Co. (DE) and Tractor Supply (TSCO) may benefit from increased support for U.S. farmers and agricultural exports. With Trump’s history of trade tariffs, there could be renewed focus on boosting domestic agricultural production, making these companies appealing for investors.

Agricultural support could include subsidies, tax relief, or other forms of assistance, which would improve the profitability of firms focused on farming equipment, crop production, and rural infrastructure. Additionally, if inflation drives up commodity prices, agricultural companies may benefit from increased crop prices and demand for machinery and equipment.

Conclusion

President Trump’s return to the White House brings with it a unique set of challenges and opportunities for investors. Inflationary pressures appear likely, driven by fiscal spending, tax cuts, and an accommodative Fed policy. While the potential for a recession or market instability exists, especially if inflation runs too hot, there are asset classes that could thrive in this environment.

For retail investors, a balanced approach focusing on hard assets, energy, financials, and select technology and industrial stocks may offer resilience and growth. Cryptocurrencies like Bitcoin and gold can provide inflation protection, while traditional energy and financials benefit from Trump’s pro-business policies. Investors should remain adaptable and informed, monitoring developments closely to make adjustments as needed.

As 2025 unfolds, the financial landscape may shift quickly. Staying diversified and vigilant, while being responsive to policy changes, can help navigate the complexities of investing under President Trump’s new administration.

As we come to the end of the blog post, here are some questions for you to ponder about:

- How much risk are you willing to take on in pursuit of growth, and are you prepared to adjust your portfolio if inflation spirals or markets turn volatile?

- With the shifting economic landscape, is it more important to focus on traditional hard assets for stability or to embrace emerging sectors like crypto and tech for potential high returns?

- How might your investment strategy change if Trump’s policies face strong resistance or if unexpected geopolitical events reshape the economic outlook?

Let me know your answers in the comments below!

After trading for 18 years, reading 1500+ books, and mentoring 1000+ traders, I specialise in helping people improve their trading results, by using tested trading strategies, and making better decisions via decision science.